Despite the fact that banks and credit unions have talked about the importance of cross-selling for decades, many still seek the best way to deepen banking relationships with depositors and borrowers.

Few institutions have a disciplined process to take advantage of cross-selling opportunities that can grow operating revenue from existing customers. For those organizations that do have a process in place, studies show that many are not targeting the offers to reflect insights readily available, thereby annoying some of their best customers.

Regardless of financial institutions’ definition – or preferred term – for cross-sell, they can only create revenue by adding new customers or by deepening existing relationships. At a time when competition for new customers has never been greater from both traditional and non-traditional players, the only sustainable opportunity is to sell more to current customers.

While findings differ some between study, research shows that U.S. adults own between 8-12 financial products each, with ownership of services increasing with age (until age 54), by channel (online users have more products) and by type of institution (credit unions and smaller banks do better cross-selling).

While the number of products held by a typical household hovers around 10, most customers only hold 2-3 services at any one institution. Only the very best organizations sell more than four services to any one customer (not including ‘go with’ services such as debit cards).

How can banks improve their penetration within their current customer base?

According to a Gallup U.S. Retail Banking Survey, which asked 9,000 financial service customers how they engage with their bank when they purchase a product or service, one in every five customers opened a new account or signed up for a new service from their bank in the last six months. The vast majority of these sales (59%) came from customers who already planned to open an account or buy a new service.

For 59%, the bank did not need to convince them of a need for a financial product. Another cohort of potential customers (33%) were considering opening an account but needed additional prompting. The smallest segment (8%) were not considering opening an account, but did so with some prompting.

What is important about the 33% of customers who are considering buying a product, but hesitate until they receive something from the bank or are talked to, is that the bank that ‘wins’ is usually the bank that understands the timing of the decision, has the best relationship and knows the offer that will best resonate with the potential buyer.

Not to be ignored are the 13% of the customers who Gallup found at one time considered buying an additional product or service at the bank, but opted not to do so. These are lost opportunities as well.

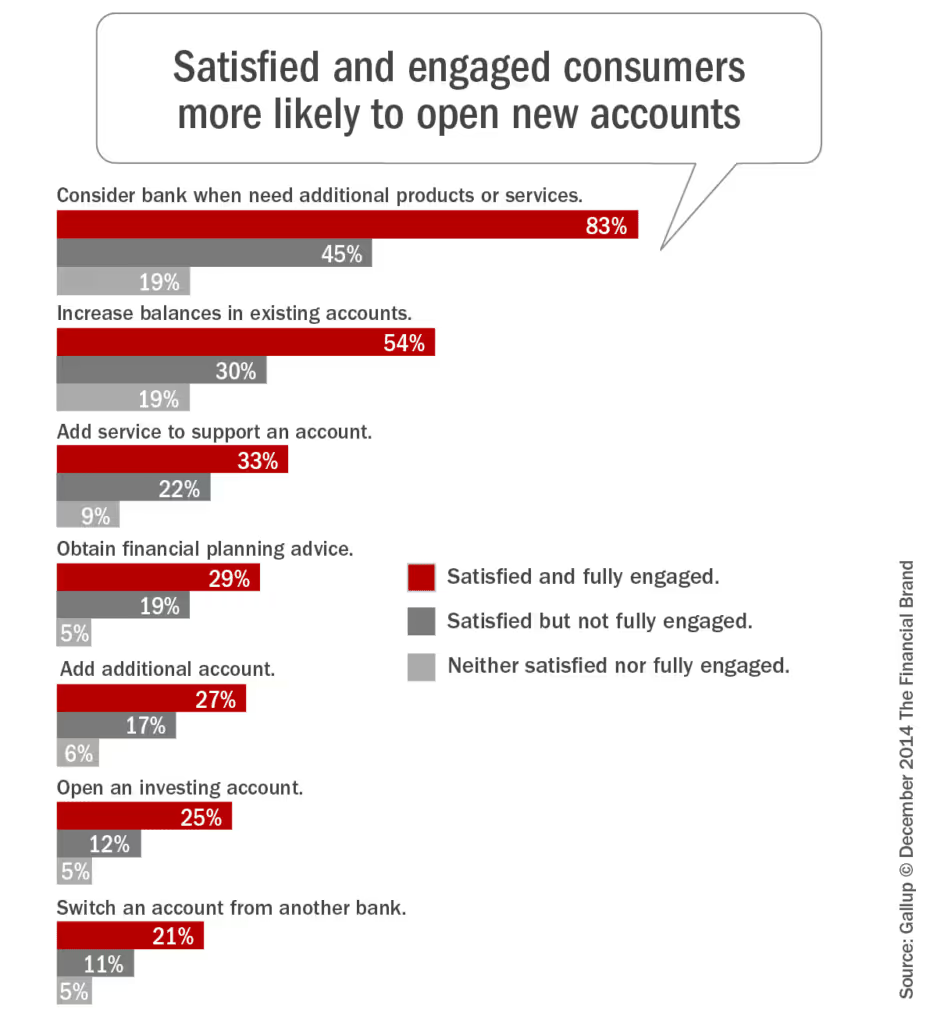

Gallup also found that customers who are ‘fully engaged’ with a financial institution are much more likely to buy an additional product from the bank or credit union than those who are just ‘satisfied’. This makes sense when you consider that a customer could be very satisfied with a financial institution that they have an account with but don’t do much with the account (mortgage only customers, CD customers without checking accounts, etc.).

For example, while less than 45% of ‘satisfied’ households surveyed by Gallup said they would consider their institution for their next product or service, that consideration increased to 83% among those who were both ‘satisfied and fully engaged.’

More than 1 in 2 ‘satisfied and fully engaged’ consumers would increase accounts. It drops to less than 1 in 3 in ‘not fully engaged,’ even when the consumer is still ‘satisfied.’

Outcomes banks desire increase with engagement: Open new accounts, adding ancillary products and services, and obtaining planning advice.

Engaged customers or members are the most likely – even more than satisfied consumers – to deepen their relationship with a financial institution. The next questions are:

- What does engagement mean to financial consumers today?

- How can institutions show up when and where their customers are engaged?

For answers to these questions, read “Cross-Sell: How Banking Consumers Engage,” the second of our three-part series on banking cross-sell by Jim Marous.

Editor’s note: Italics indicate edits to the original to accommodate layout or to provide additional information or resources for this series.