This week, the Minnesota Mortgage Association held its 2017 Annual Convention & Awards event in downtown Minneapolis. Total Expert Founder and CEO, Joe Welu, presented “Generating Leads Through Social Media” along with Andrea Kozek, MGIC’s Digital and Social Strategist. If you didn’t attend, you can hear Joe’s take on this critical business activity in our Expert Strategies podcast. It was also great to talk with loan officers about their practices and challenges, and we heard from several MLOs that Realtor enthusiasm is suffering due to low inventory.

A prevalent Realtor attitude seems to be, “Why try to get more leads if I don’t have anything to sell them?” This uninspired mindset provides an opportunity for MLOs to “come to the rescue” and be part of the solution to the low inventory doldrums by helping agents pursue potential business sources they don’t necessarily tap on a regular basis – or to their full potential. Market and news developments provide great conversation starters and compelling data that can create receptivity among different contact and prospect types to consider options they may not realize they have. MLOs can reach out to Realtor partners and prospects with ideas and assistance in approaching different groups with compelling, current information that could help generate inventory and sales.

Expired Listings

Whether the sellers were asking too much or they weren’t truly committed to making a move, these homeowners can benefit from current market data and mortgage reviews. Their homes may have appreciated and equity increased since their non-productive time on the market.

For Sale by Owner (FSBO) Listings

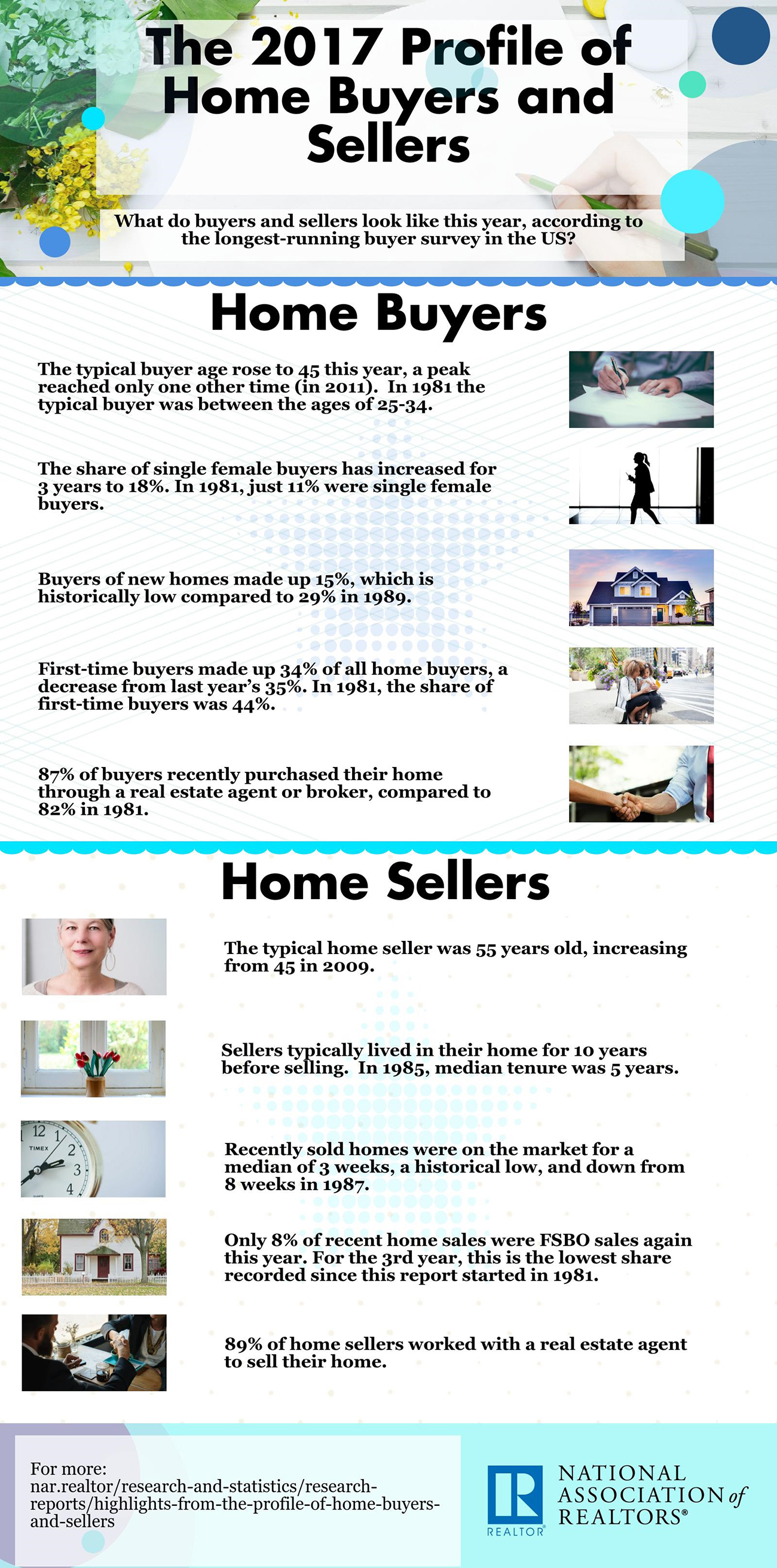

People who put a sign in the yard with the hope of avoiding real estate commissions might have a change of heart after seeing the following facts from the National Association of Realtors (NAR) 2017 Profile of Home Buyers and Sellers:

- The median sold price of For Sale by Owner properties was 24% less than the median agent-assisted property sold price.

- More than half of FSBO properties that sold were to buyers that the sellers knew.

FSBO sellers who don’t have a buyer waiting in the wings might be open to at least paying a buy-side commission.

Make Me Move (Zillow)

A lot of real estate pros use Zillow to advertise, but you can also find potential sellers by sifting through a listing type on the site called “Make Me Move.” This feature allows homeowners to promote their properties by adding photos, video and other data along with a price they would accept to move. In addition to agents pursuing these owners as potential listings, MLOs can reach out and discuss future goals, such as financing for their next home if a sale were facilitated. Homeowners dabbling with this Zillow feature may be surprised at how they can leverage equity for their next move and possibly fund other goals.

Databases: Past Client, Sphere of Influence

The concept of “what it would take to make a homeowner move” is a question all homeowners with equity should consider. Realtors and MLOs should be asking this question in their regular outreach to their contacts. Homeowners who are currently content may find that the reasons they’ve been staying put are no longer valid, or something they’ve been waiting for, such as a certain amount of value appreciation has arrived.

Reaching out to these four groups with solid, current information adds value to consumers and Realtor partners. Whether MLOs schedule working sessions and make calls with agents or they present these ideas and messaging in a setting like a Lunch & Learn, offering to get into the trenches and do the work to develop business can help create powerful bonds that extend beyond mental or market funks. Some Realtors balk at the idea of co-marketing during slow times, but that’s precisely when they should be digging in, especially with a lending partner who isn’t beleaguered by frontline market challenges like low inventory.

Even with the winter season approaching, a proactive co-marketing plan backed by tools and the encouragement of a business partner can change attitudes and production numbers. This also builds trust and a great foundation for broader co-marketing efforts on a long-term basis.

Regardless of how Realtors may be feeling right now, MLOs need to prepare for what’s on the horizon: The Mortgage Bankers Association forecasts that purchase business will increase at a faster clip in 2018 – nearly double the rate that it increased in 2017. Set the stage for a productive new year by helping Realtors tackle challenges they’re facing today.

{kind=link}